The Original Goal of Bitcoin was not the 21-Million Cap

Satoshi Nakamoto did not invent Bitcoin to create a fixed-supply commodity, but to bring electronic cash to the world.

This post is a translation of an article I wrote in French.

When someone learns about Bitcoin, it doesn’t take long for them to find out that its issuance is reduced over time and that the total supply is capped at 21 million coins. They are subsequently led to conclude that if its use grows, then the value of bitcoin will skyrocket due to its absolute scarcity. This is the speculative logic that led its price to rise from $0.001 to $126,000 in less than 20 years.

However, the iconic 21 million cap—now championed by all sorts of hucksters—was not the original goal of Nakamoto’s system and has been secondary throughout its development; it was long considered a means to make bitcoin attractive, not an end in itself. The most striking proof of this fact is that Bitcoin was originally designed to have a constant money issuance schedule. Satoshi Nakamoto implemented the halvings and the supply cap only after the white paper was published.

Now that the Saylorian mysticism is prevailing, now that ETFs are proliferating, now that the most powerful state on Earth is building a bitcoin strategic reserve, perhaps it’s worth remembering that Bitcoin’s initial purpose was far nobler than simply attracting every greedy soul on earth.

A Tale of Two White Papers

On October 31, 2008, Satoshi Nakamoto unveiled his discovery by sending the Bitcoin white paper, titled Bitcoin: A Peer-to-Peer Electronic Cash System, to the Metzdowd.com cryptography mailing list. This document, however, is not the only version that ever existed; he published another, updated version of the paper on March 24, 2009, which is hosted on Bitcoin.org and to which we generally refer today. The first white paper thus differs slightly from the second.

In particular, in this first document, Satoshi did not mention the “transaction fees” or the “predetermined number of coins,” as he would later. To reward miners who ensure payment processing, he provided for constant money issuance, presumably 100 bitcoins every 15 minutes1. In the white paper, he wrote:

“The steady addition of a constant of [sic] amount of new coins is analogous to gold miners expending resources to add gold to circulation.”

He thus justified the choice of “natural inflation” by comparing bitcoin to gold, which has always experienced some monetary creation while maintaining its purchasing power2. With a constant quantity of new bitcoins, the annual issuance rate should decrease over time: it would fall below 5% after 20 years, and below 2% after 50 years. Beyond the white paper statement, Satoshi clarified in a private email a few days later:

“The supply of gold increases by about 2%–3% per year. Any fiat currency typically averages more inflation than that.”

Conversation with Ray Dillinger

In November 2008, Satoshi discussed Bitcoin with members of the mailing list. In particular, he exchanged messages with Ray Dillinger, an independent consultant in new technologies, who was interested in digital currency protocols. In an email sent in the evening of November 5 (PST), Dillinger criticized bitcoin for its “lack of intrinsic value,” failing to fully understand that it is a defined monetary policy, controlled by a difficulty adjustment algorithm. For his view, anyone could create new coins indefinitely (as in Hal Finney’s RPOW system), which considerably reduces the currency’s value. He concluded incorrectly that the currency was “inflationary at about 35% as that’s how much faster computers get annually.” Satoshi debated this with him privately, before correcting him publicly on November 8:

“[T]he difficulty increases proportionally to keep the total new production constant. Thus, it is known in advance how many new bitcoins will be created every year in the future.

The fact that new coins are produced means the money supply increases by a planned amount, but this does not necessarily result in inflation. If the supply of money increases at the same rate that the number of people using it increases, prices remain stable. If it does not increase as fast as demand, there will be deflation and early holders of money will see its value increase.

Coins have to get initially distributed somehow, and a constant rate seems like the best formula.”

Satoshi confirmed the existence of this initial design to Martti Malmi in May 2009 in an email including his private debate with Ray:

“This inflation discussion was before the transaction fee mechanism and fixed plan of 21 million coins was posted, so it may not be as applicable anymore.”

However, this design was flawed, a fact that Bitcoin’s first critic—James A. Donald—was quick to point out.

Exchange with James A. Donald

James A. Donald is an anonymous cypherpunk who was the first to respond publicly to Satoshi, on November 2, to criticize Bitcoin for its lack of scalability. The two men exchanged at length on the mailing list. It was the Donald’s comments on Bitcoin’s incentive structure that prompted Satoshi to rethink its monetary policy and incorporate transaction fees.

In the night of November 8 to 9, James A. Donald blamed the constant money issuance schedule chosen by Satoshi for incentivizing miners to ensure transaction processing. He nevertheless nuanced his statement by adding that it is better than traditional currencies subject to the vagaries of policy:

“[I]t cannot be made to work, as in the proposed system the work of tracking who owns what coins is paid for by seigniorage, which requires inflation.

This is not an intolerable flaw - predictable inflation is less objectionable than inflation that gets jiggered around from time to time to transfer wealth from one voting block to another.”

The same day, James A. Donald raised a new criticism, this time on the fact that a miner is not incentivized to include transactions in a block:

“This solution … does not solve the spend recording problem. If one node is ignoring all spends that it does not care about, it suffers no adverse consequences.”

This discussion gave Satoshi the idea to add a transaction fee mechanism to Bitcoin, which would solve both problems at the once. In the evening of November 9, responding to James A. Donald, he described this mechanism as follows:

“If you’re having trouble with the inflation issue, it’s easy to tweak it for transaction fees instead. It’s as simple as this: let the output value from any transaction be 1 cent less than the input value. Either the client software automatically writes transactions for 1 cent more than the intended payment value, or it could come out of the payee’s side. The incentive value when a node finds a proof-of-work for a block could be the total of the fees in the block.”

The next day, Satoshi added:

“With the transaction fee based incentive system I recently posted, nodes would have an incentive to include all the paying transactions they receive.”

November 2008 Code

Following this exchange with James A. Donald, Satoshi Nakamoto decided to implement the transaction fee mechanism into the Bitcoin design. He also reduced money issuance over time, so as to limit the supply to a predefined amount. On November 14, in a response to Ray Dillinger, he wrote:

“There will be transaction fees, so nodes will have an incentive to receive and include all the transactions they can. Nodes will eventually be compensated by transaction fees alone when the total coins created hits the pre-determined ceiling.”

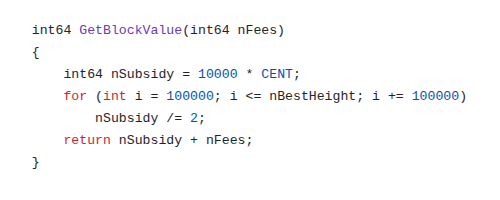

On November 16, he shared the Bitcoin software code with some members of the mailing list, including Ray Dillinger and James A. Donald. The parameters in this version differ from the January 2009 prototype. The time between each block, for example, is 15 minutes (instead of 10). Each coin is divided into 100 cents, which are themselves divided into 10,000 smaller units, so that one bitcoin corresponds to 1 million base units.

Most notably, Satoshi included the halving mechanism, which divides money creation by two every 100,000 blocks, or approximately 2 years and 10 months. In this version of the code, 100 bitcoins are created during the first 100,000-block period, 50 during the second period, etc., so that the total quantity of bitcoins converges toward 20 million coins, which would be reached 77 years later.

Network Launch

A month and a half later, on January 8, 2009, Satoshi Nakamoto published version 0.1 of the software. This included the parameters we are all familiar with: the 10-minute block time, the 50-bitcoin block subsidy, the 100 million base units (”satoshis”) per coin, the 4-year halving, and the 21 million bitcoin cap. As he wrote a few months later to Mike Hearn, the choice of the 21 million number and unit granularity was an “educated guess”—”something in the middle” that would allow for both the scenario where Bitcoin would remain a “small niche” and the scenario where it would be used “for some fraction of world commerce.”

Beyond the code, Satoshi described the final monetary policy in his introductory email:

“Total circulation will be 21,000,000 coins. It’ll be distributed to network nodes when they make blocks, with the amount cut in half every 4 years. … When that runs out, the system can support transaction fees if needed.”

On January 10, Hal Finney, an American engineer known for his involvement in the cypherpunk movement and in Phil Zimmermann’s PGP, endorsed this approach, enthusiastically noting that “the system can be configured to only allow a certain maximum number of coins ever to be generated.” In his email, he estimated that if Bitcoin became “the dominant payment system in use throughout the world,” that would give each coin “a value of about $10 million.”

Satoshi saw this prediction as a powerful marketing tool to make people want to try Bitcoin. He thus used this selling point repeatedly, on the cryptography mailing list in January and on the P2P Foundation forum in February. And it had the desired effect: Dustin Trammell, one of the first miners after Satoshi and Hal, told Bitcoin’s creator that this opportunity to make money was “was one of the other reasons [he] started up a node so quickly.”

Satoshi subsequently distanced himself from the speculative element, hardly ever speaking of it and always in very measured terms. In June 2009, in an email to Martti Malmi, he wrote that he was “uncomfortable with explicitly saying” that bitcoin should be considered “an investment,” arguing that it was a “dangerous thing to say” (from a legal standpoint presumably). He added:

“It’s OK if they come to that conclusion on their own, but we can’t pitch it as that.”

But the public’s imagination had already been irrevocably influenced, and the successive bubbles that occurred in 2011 and 2013 completed the shift in the general perception of Bitcoin.

Bitcoin has been Corrupted

Satoshi Nakamoto was therefore not opposed to people using bitcoin as a store of value, as “a long-odds investment.” But he saw this speculative logic more as a means to economically bootstrap his system than as an end in itself. Satoshi Nakamoto’s main goal, explicitly stated in the white paper introduction, was to solve the problem of online payments by creating a form of “electronic cash” that could be used “without the need for a trusted third party.”

He considered that his système was ready on October 31, 2008, because his objective could be achieved with a constant money issuance schedule. He revised this aspect since the transaction-fee/fixed-supply design was simply more elegant: fees incentivize miners to include transactions in their blocks while “natural deflation“ rewards merchants who hold onto the coins they receive, limiting exchange with traditional currencies. The second design was therefore much better suited to fulfilling Bitcoin’s original purpose.

It’s hard to deny that the speculation induced by the 21-million cap has been the key factor enabling Bitcoin to survive to this day. Among other things, it guaranteed a minimum demand for the coin and a floor level of network usage. But this pursuit of profit has gotten out of hand to the point where it no longer truly serves Bitcoin’s healthy development, in the sense that people no longer even take custody of their own bitcoins. Satoshi Nakamoto originally intended to create a “peer-to-peer electronic cash system,” not a “digital commodity without an issuer” that would serve as backing for institutional financial instruments or as collateral in secured loans. It might be opportune to remember this.

This article is a reworked and expanded version of several sections from the course on The History of Bitcoin’s Creation published on PlanB Academy. The illustration was created using GPT Image 1.5, based on the 20th Century Fox logo; the idea came from u/birth_of_bitcoin on Reddit. This post was translated from French using Kimi K2.5 and then revised by myself.

This design inevitably recalls Monero’s tail emission, which is 0.6 XMR every two minutes.

Despite the conception supported by some Austrian economists like Ludwig von Mises, monetary inflation does not equal price inflation, as economic growth partly compensates for money creation. In the case of a commodity money subject only to the market, there is no price inflation, unless the conditions of its production change drastically.

Good article for history..